A corporate reorganization rarely changes only the boxes on an org chart. When shares are exchanged, redeemed, or reallocated among owners, the underlying economics of the business shift with them, and those shifts must be captured before anyone can rely on the numbers. A dependable company valuation report starts long before the final figure is calculated. It begins with disciplined documentation of every shareholder adjustment, because a reorganization that looks tidy on paper can hide material changes in control, entitlement, and risk that directly affect what the business is worth.

Why Shareholder Adjustments Change the Numbers

Reorganizations move value around even when the total enterprise value stays constant. A freeze that converts common shares into fixed-value preferred shares, a family trust added to the ownership chain, or a buy-out that shifts a minority holder into a control position all alter how value is allocated among the parties. Ownership structure and the rights attached to each share class determine how equity is reallocated during a restructuring, and getting that allocation wrong can produce real losses for one party at the expense of another. Fair share exchange ratios exist precisely to prevent that kind of imbalance.

The effect is not only about headline value. It is about the specific adjustments a valuator applies to reach fair market value for a particular block of shares. Control and minority positions are not valued the same way, and liquidity varies across share classes and shareholders. A credible report reflects these realities rather than treating every share as identical, and it explains the reasoning behind each adjustment so that a reader can follow how the final figure was reached.

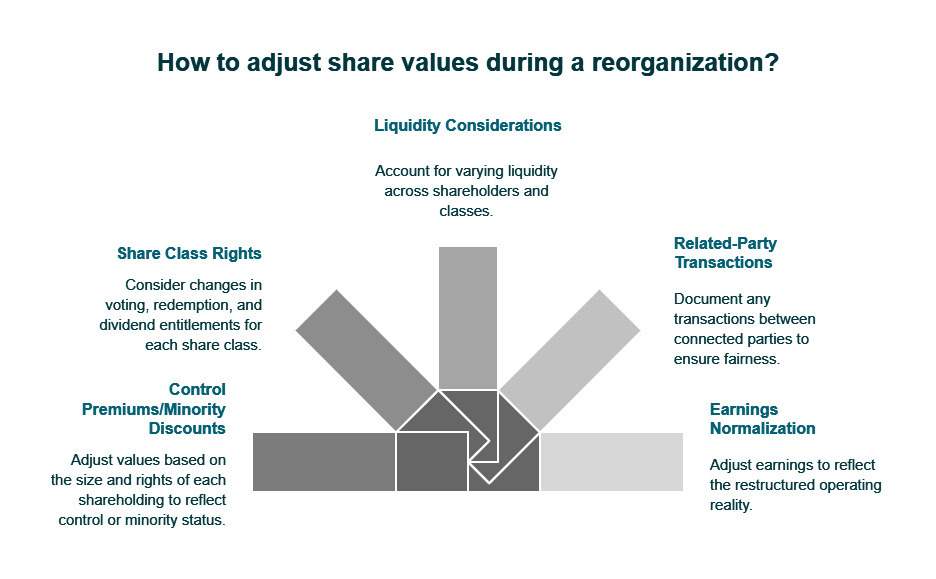

Common adjustments that need to be documented during a reorganization include:

- Control premiums or minority discounts tied to the size and rights of each shareholding

- Changes in share class rights, including voting, redemption, and dividend entitlements

- Liquidity considerations that differ across shareholders and classes

- Related-party transactions where shares or assets move between connected parties

- Normalizing adjustments to earnings that reflect the restructured operating reality

Building the Documentation Trail

The strength of a valuation depends on the quality of the record behind it. Financial statements, ownership registers, shareholder agreements, and corporate resolutions together explain who owns what, and why the structure looks the way it does after the reorganization. When those documents are gathered and reconciled early, the valuator can apply fair market value approaches to the affected entity or division with confidence, and the resulting conclusions can withstand later scrutiny.

That scrutiny is real. When shares or assets change hands between related parties, or a structure is altered for tax purposes, tax authorities such as the CRA expect defensible, independent valuations that support the reported figures. Clear documentation also reduces the risk of disputes among shareholders, lenders, and family members, because each adjustment can be traced back to a source document rather than resting on assertion. Independent valuations carry particular weight here, since a report prepared at arm’s length is less open to the claim that it was shaped to favour one shareholder. A well-supported trail turns a valuation from an opinion into a position that can be defended when questioned.

Turning Documentation into a Defensible Conclusion

Once adjustments are recorded and reconciled, the valuator selects the approach that fits the situation, whether an income approach built on discounted future cash flows, a market approach anchored to comparable transactions, or an asset-based approach where the circumstances call for it. The documentation informs the assumptions behind each method, from the normalized earnings base to the discounts and premiums applied to specific shareholdings. A conclusion that can point to its supporting evidence at every step is far harder to challenge than one that cannot, and it gives everyone involved a clearer view of how the result was built.

This is where careful preparation pays off. A report grounded in a complete record does more than satisfy a regulator. It gives owners, boards, and their advisors a reliable basis for decisions about buy-outs, tax planning, and future transactions, and it holds up if the reorganization is ever revisited in a dispute or an audit years later.

At Valuation Support Partners, documenting shareholder adjustments with rigor is central to producing valuations that clients and their advisors can stand behind. Whether the reorganization involves a share transaction, a shareholder buy-out, or an internal restructuring for tax and estate planning, a carefully built record is what separates a number on a page from a valuation that carries weight when it truly matters most.